Equity distribution in early-stage startups is a slightly odd subject. Obviously at this point the startup is worth nothing – or less-than-nothing, if expenses are being recorded as debts on the future company – and who wants to argue about percentage points of nothing? Sometimes the whole subject is just ignored.

On the other hand, whatever the addressable market size of the idea at hand, the spectre of founders squabbling over enormous wealth is lurking somewhere in the subconscious of everyone involved, so it is equally possible to go the other way, and invoke complex calculation methods of one kind or another, however irrationally over-fussy.

While complex approaches are arguably better than failing to address the issue at all, a simpler method is more typically adopted: if there are two founders at the beginning, they are usually assumed to have 50% each, if three, 33 1/3%, etc – as in this Seedcamp agreement template.

If they add additional co-founders, there is a re-distribution by agreement, such that the original co-founders see their percentage ownership reduced, to ‘make room’ for the new partner. The process is repeated each time a new equity-holder is added (ignoring such things as special share types – usually considered as over-complicated at early stages).

I consider that there are several problems with this:

- Bad psychology A: by allocating all the equity at the outset, there is a subtle implication that the situation is settled. Of course, everyone knows intellectually that the hard work to make the idea worth something in the world is all to come, but nevertheless, there is the potential for a ‘Tragedy of the Commons’ mode of thinking (a rationally selfish decision to freeload where possible on the efforts of the other partners) which is obviously unhelpful.

-

Bad psychology B: each new equity-holder added appears to the existing members as someone who, no matter what they bring to the project, is taking something from them, as their share is necessarily diluted. However much they might intellectually understand that 50% of nothing is less than 10% of something, this feeling is not a positive one.

-

Bad Psychology C: ‘the ‘cliff’. This term relates to ‘Vesting’ (discussed below). Simply, it means that anyone who leaves the company before the agreed ‘cliff’ time-period since the founding date has passed gets no equity – anything that they were supposed to get does not ‘vest’, because they didn’t stick around. This period is typically a year, and the policy is obviously intended to ensure maximum commitment during this early phase. One problem is the potential for ‘Bad Leaver’ issues, as discussed below. The other problem is the person who loses interest after 9 months but wants to get their chunk of equity – again, rational self interest encourages them to do the minimum necessary to stay engaged for three more months, then cop out – at which point they might have 30% or more of the equity.

- Bad leaver problem: A ‘Bad leaver’ is anyone who leaves the company under disputatious circumstances. Under the typical arrangement, if this person is one of the early founders, they might leave with anything up to 50% of the equity. Given that a dispute exists, it is likely that the remaining active members will resent this – there will often be an argument as to whether the holding is fully deserved, which could lead to court action, or the threat of such – to the inevitable detriment of the company.

An Incremental approach to equity distribution

Under this approach, the co-founders agree on a percentage of the equity which they will consider as their due for founding the project – typically 5-10% (this may be the same for everyone, or otherwise as agreed). The remaining equity will be considered to be ‘unallocated’ (this is handled in different technical ways in different jurisdictions – I Am Not A Lawyer alert!).

Additional equity increments are awarded as decided by the founders/board. Typically, increments will be small – generally less than 3% – issued at agreed stages (periods of time or particular milestone events) on the basis of two metrics: achievement of agreed tasks/goals being the most important, the other relating to persistent commitment of time and effort.

A new partner coming into the business will be allotted an initial tranche of equity as a ‘welcome’ – typically less than the initial founders – depending upon how much work they have already done.

This approach addresses the perceived problems in a fairly obvious way:

- Bad psychology A: by making it clear that final equity shares in the future will be in direct proportion to agreed contribution to the development of the enterprise, individuals are encouraged to align fully with its progress.

- Bad psychology B: share allocations to others do not alter any individual’s understanding of his/her percentage holding in the company.

- Bad psychology C: the incremental approach deals with this problem – by reducing time periods and equity tranches, anyone who loses interest can go pretty much straight away, confident that what they have earned through full engagement remains theirs, with no incentive to ‘game the system’.

- Bad leaver problem: the ‘Bad leaver’ goes with no more than the previously allocated portion of the equity – which is less likely to be the subject of dispute as it has been assessed and agreed at each increment on the basis of real contribution.

Some Details

Obviously the detailed implementation of this approach needs to be enshrined in some documentation – either a pre-incorporation agreement or in the founding documentation of a formalised company, but beyond that, let’s consider some specific features.

This approach requires the founders to spend at least some minimum amount of time in formal planning, setting out and recording roles, expectations, targets, milestones etc, as appropriate. This is a Good Thing.

If some analogue of an Agile approach is being used, then the time periods and product increments adopted when work planning should obviously relate tightly to the periods and criteria adopted for agreeing equity allotment.

It should be noted that two types of performance are to be recognised: firstly, diligent work for the furtherance of the project – irrespective of whether specific targets or events are met – and secondly, achievement of specific targets or milestones. Thus commitment can be rewarded, even if things are harder or slower than imagined.

In the case of a decision requiring majority voting, unallocated shares are voted in proportion with allocated equity.

Vesting

Vesting describes a future entitlement to shares, based either on continued engagement with the project or on agreed achievements.

Vesting is more widely used in the US, although not unknown in the UK, but is generally understood to bring share allocations on the basis of continued employment in the business.

The approach described here is more about agreed achievements – it may also make sense to delay vesting of allocated share increments by one or more time periods, to encourage continued commitment and further reduce scope for later argument.

Investors

At some early stage the equity holders should come to a view as to the proportion of equity to be provisionally allocated for cash investors. This will vary from venture to venture, but again, the aim is to set up a situation where at least the first couple of investment rounds are not experienced as dilutions by existing equity holders.

Later stage investment is of a different character, and may well require dilution, but by this point the business should have entered a different phase, where the value of equity can increasingly be measured by external yardsticks, and is no longer in startup mode.

An example

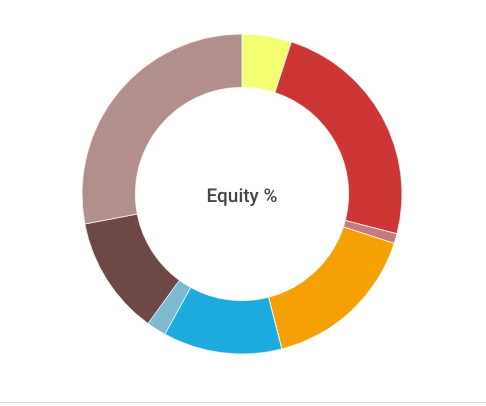

If all this seems complex, here’s an example which will clarify things. In the image, the pale yellow is unallocated partner equity, the grey is unallocated investor equity. Brighter colours represent Alice, Bob and Charles – strong for ‘vested’ and paler for ‘allocated’.

Alice and Bob dream up a great idea one lunchtime. After some soul-searching, they quit work to see if their idea can swim in the great wide world.

They decide to award each other 5% each of the equity, and to set aside 40% of the equity for early investors. Thus 50% of the equity is notionally unallocated at this point. They further agree that earned equity allocations will not ‘vest’ until the end of the following timebox.

They come up with a plan of campaign, and decide to work in 6 week timeboxes. They decide that the first timebox is worth 2% if each of them continue to engage, with an additional 1% against some agreed targets.

At the end of the first period, all is well – they agree to a further 3% each.

Reviewing the plan, they realise everything is a little slower than they had hoped – they downgrade the next timebox to 1% +1% for commitment.

Bob is now offered some well paid contract work, and decides to take it – he can’t contribute as planned.

At the end of Timebox 2, they agree that Alice should get the full 2%, but that Bob should only get 1%. The allocation from the first timebox vests. Both now have 5+3=8%.

Timebox 3 goes on the same lines, with Bob still not able to fully commit, while Alice works on. At the end, Alice is allocated another 2%, Bob another 1. Timebox 2 allocation vests, and Alice now has 8+2=10%, while Bob has 8+1=9%.

Bob’s contract ends, and he comes back in with renewed determination. They decide to push forward hard, and that Timebox 4 is worth 3%+1%.

…and so on…

Things proceed in this way for another few periods; Alice now has 16% and Bob 14%. They agree they need a new partner with additional skills – Charles jumps at the chance. They offer him a 2% ‘welcome’, and all three revisit the project plan.

After another few months, they are at the point where they can talk seriously to an angel investor, who eventually takes 12% of the equity.

They are now ready to hire their first employee, and build out their offer to the market. Alice has 20%, Bob 16%, Charles 7% and the investor 12%.

A month later, Alice and Bob disagree seriously about whether the company needs to pivot. A nasty moment. After discussions, Charles decides that he agrees with Alice. The investor agrees.

Bob cannot commit to a company that is making a fundamental choice he feels is wrong, and takes up a job offer. This is a serious blow, but there is no argument about Bob’s equity stake in the company – it was clearly earned and allocations were agreed at every stage. He will get no further increments, of course. Alice and Charles take on another employee, and Bob wishes them well – after all, if they succeed, he might end up with a 16% stake in a successful company!